Factor Update, May 1st

This content is for members only

As a trader, my favorite chart configuration is the Head and Shoulders. The H&S pattern is easily recognizable (although for reasons I will not go into here, the novice chartist falsely finds the H&S form everywhere), produces far more reliable trading signals than more frequent patterns and is found at major turning points.

Apple has formed H&S patterns at many major turning points in recent years. The Factor has identified, alerted members and traded many of the following H&S patterns in real time.

Chart traders need to keep their eyes on Apple. The H&S pattern, when it occurs in Apple, is always worth a trade. Truly, Apple is head and shoulders above the rest.

Factor trading tactics explained

Identifying a pattern is a relatively easy task in which to gain competence. Trading a pattern once identified – now that is a horse of a different color.

How many times have you heard another trader say (or said to yourself): “I knew that stock XYZ was going to go up, and it did, but I did not make a dime on the move?”

Trade signaling, in my opinion, is far less important to net profitability than is proper trading tactics and aggressive risk management protocols.

Factor LLC, in its proprietary account, traded two of the H&S pattern featured herein as follows (adjusted for splits, not adjusted for commissions):

2015 H&S top sell signal

Shorted the close on Aug 3 at 116.68 with an initial risk to 122.31, or a risk of $5.63 per share. The target was

103.22. Factor risked 60 basis points on the trade (6/10th of 1%), or $6,000 per $1MM of trading capital. A 60 BP trade represented a 1,000 shares position (actual initial risk was $5,630 per $1MM).

The protective stop was moved to 116.82 after the close on Aug 21. Factor takes profits when targets are met. The target was exceed with a gap down open on Aug 24 at 93.98. Factor maintains open orders to take profits at target levels. The profit for the trade was

$22,700 or 227 BPs.

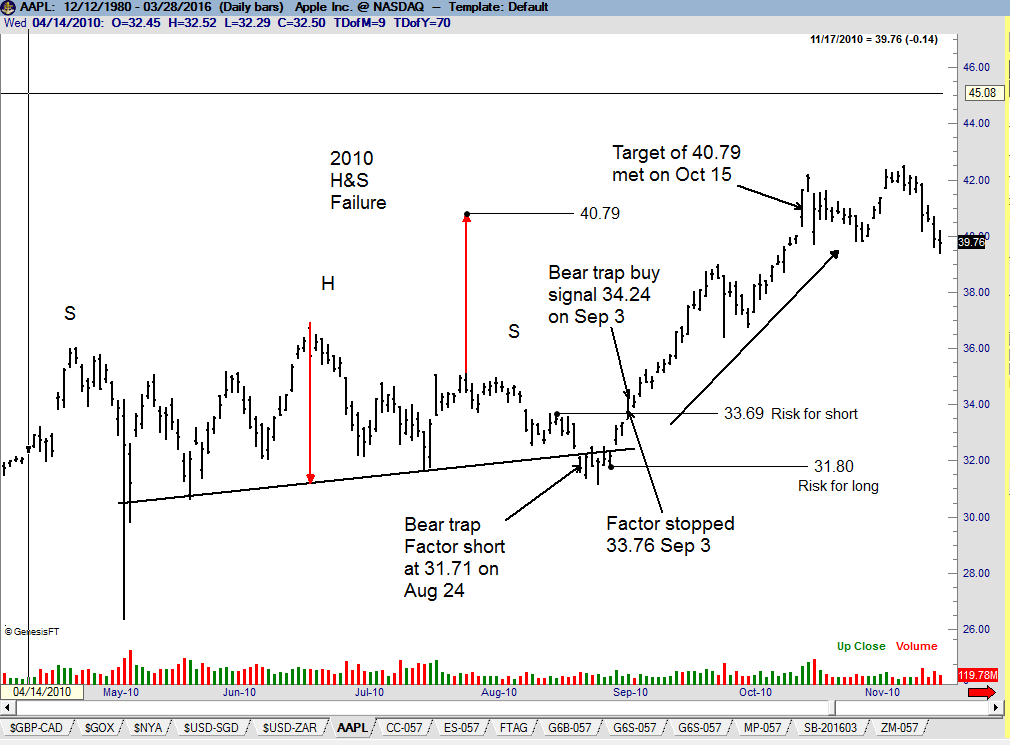

2010 H&S top sell signal — then 2010 H&S failure buy signal

34.24 with 60 BP risk to 31.79 and target of 40.79. AAPL reached target on Oct 15. The profit for the trade was $15,720 per $1MM or 157 BPs.

plb

###

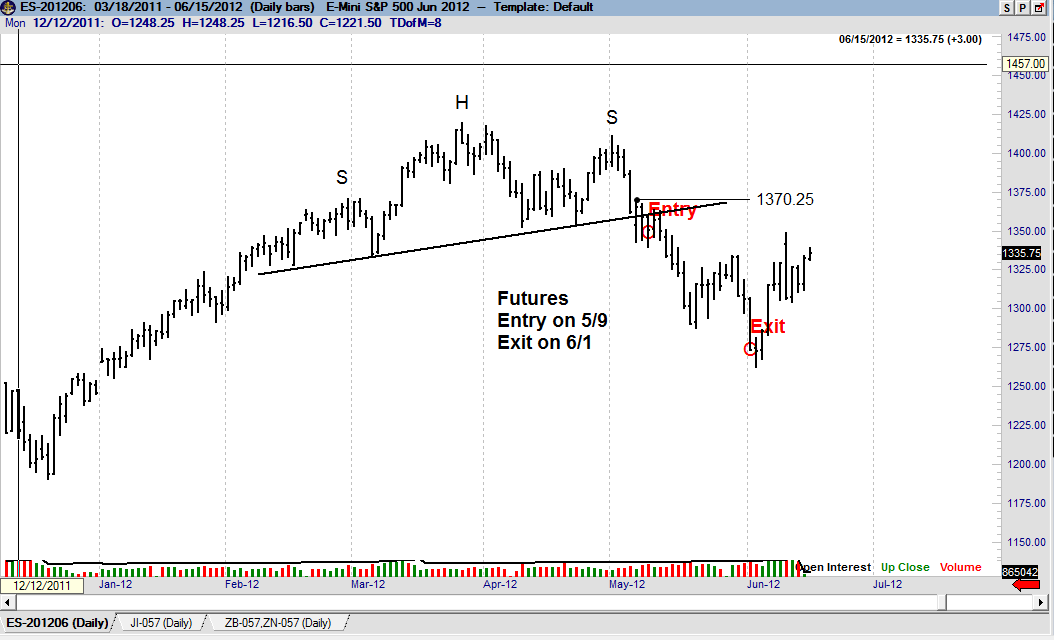

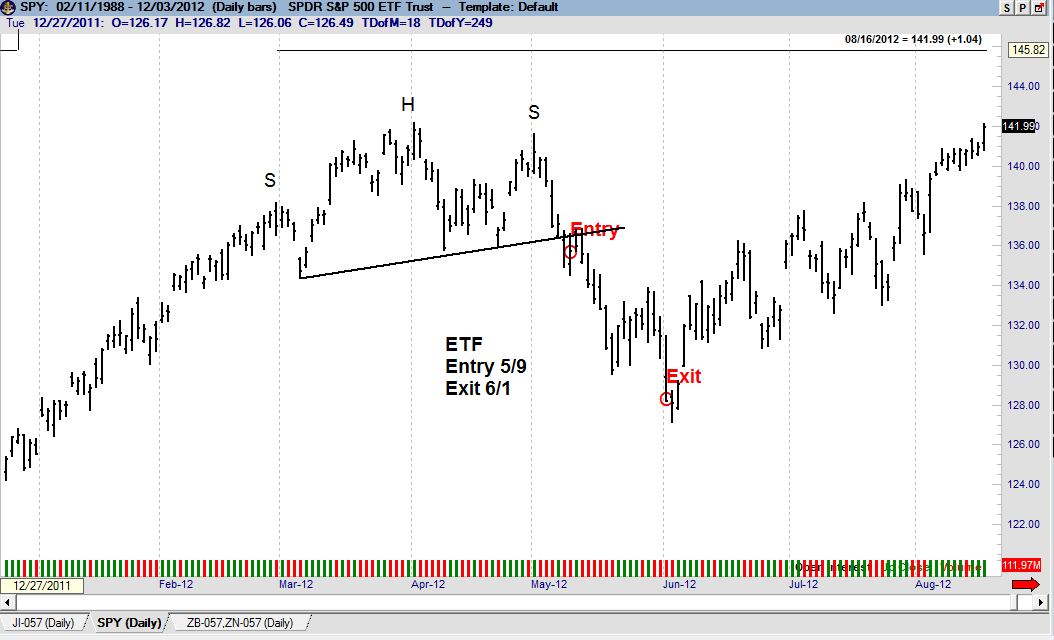

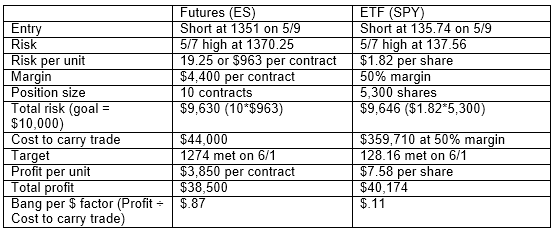

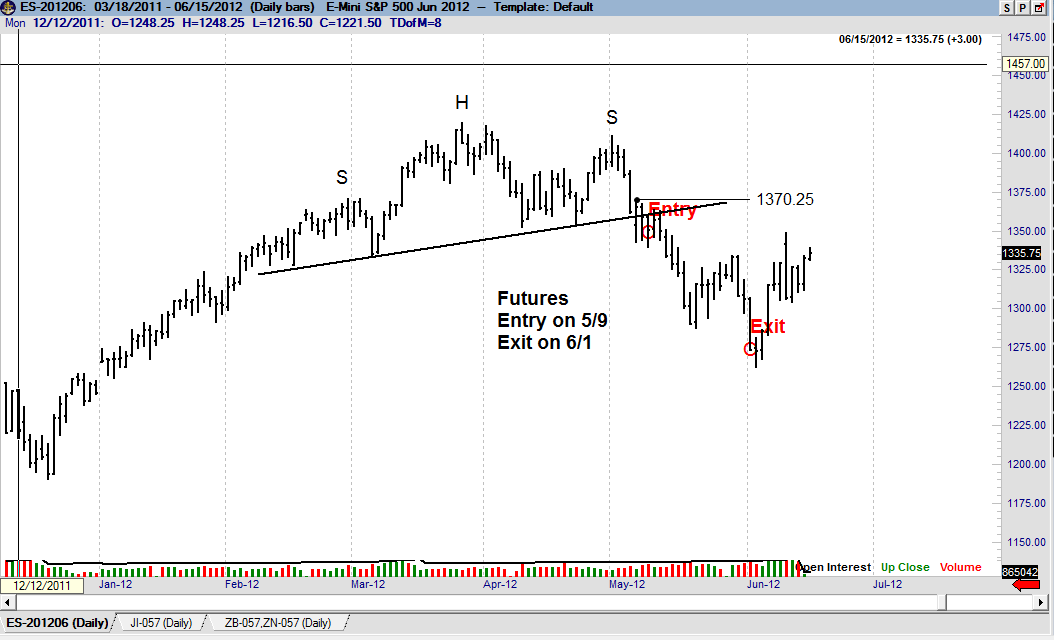

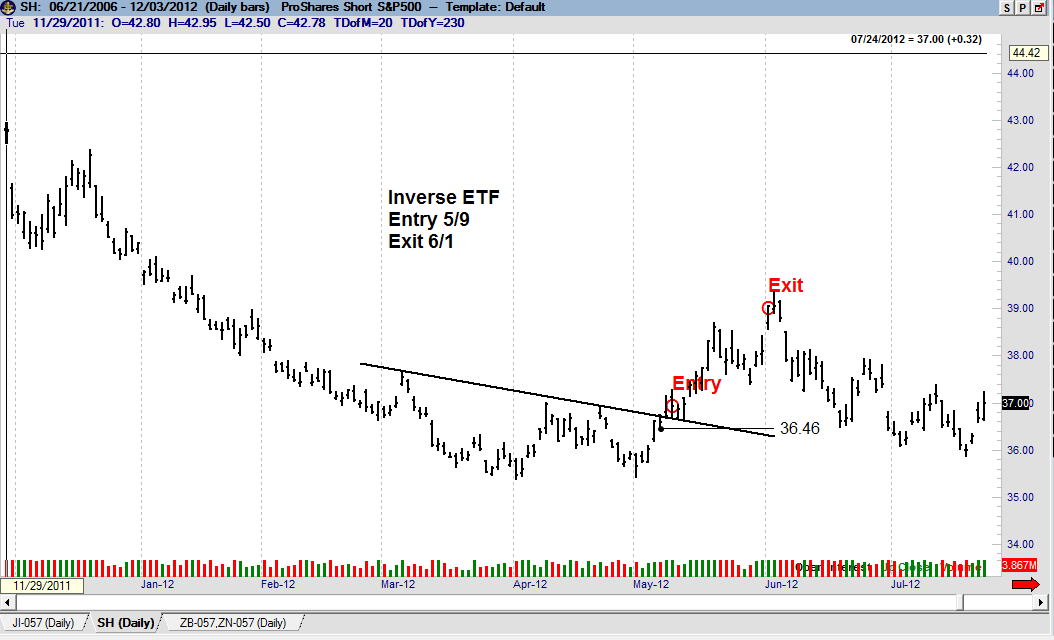

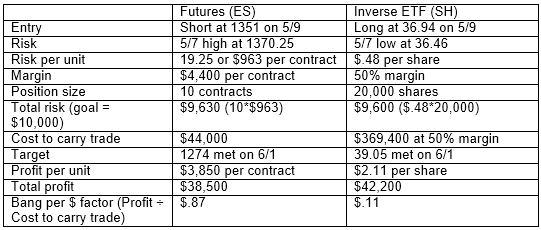

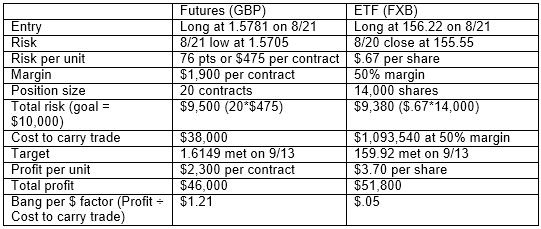

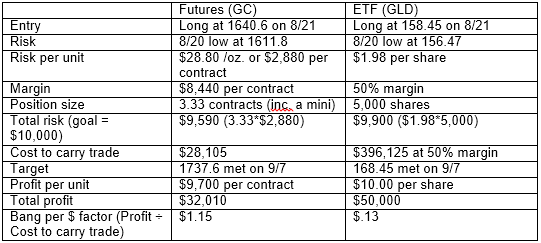

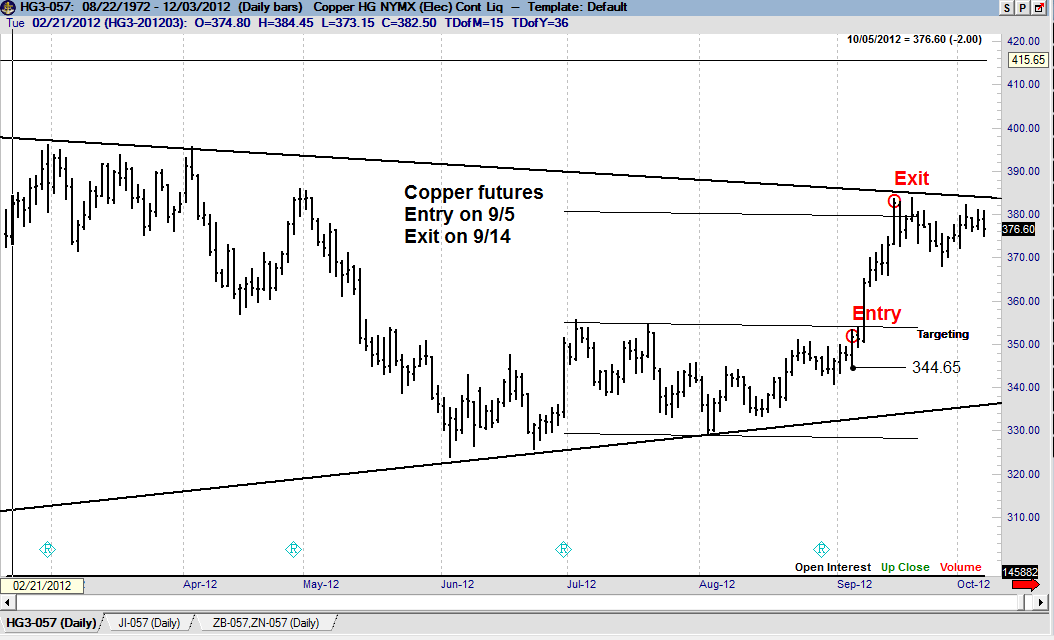

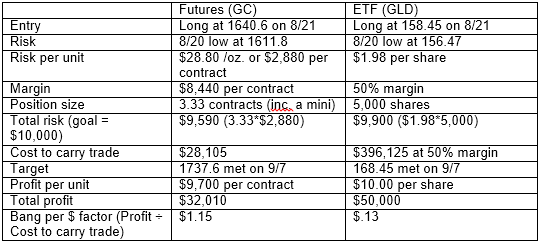

Trading an ETF tied to an underlying Futures or Forex market requires far more capital with less profit potential at the exact same level of risk as directly trading the underlying futures or forex contract. Five examples are provided to make my point.

Assumptions:

Note: This post will no doubt create some level of controversy and disagreement. This is my intent. I will stand by my position that trading an ETF tied to an underlying futures or forex market is a very foolish way to manage trading capital. I have no idea why a trader would ever trade a futures or forex-related ETF if he or she can handle the risk of the futures and forex markets. Let the facts of this document speak for themselves.

Summary: Trading SPY ties up eight times more capital in a trade with a near-identical risk to reward profile. FOOLISH!

Summary: Trading an inverse S&P ETF (SH) ties up eight times more capital in a trade with a near-identical risk to reward profile. FOOLISH!

Summary: Trading a long British Pound ETF (FXB) ties up 24-times more capital in a trade with a near-identical risk to reward profile. FOOLISH! REALLY FOOLISH! JUST PLAIN STUPID!

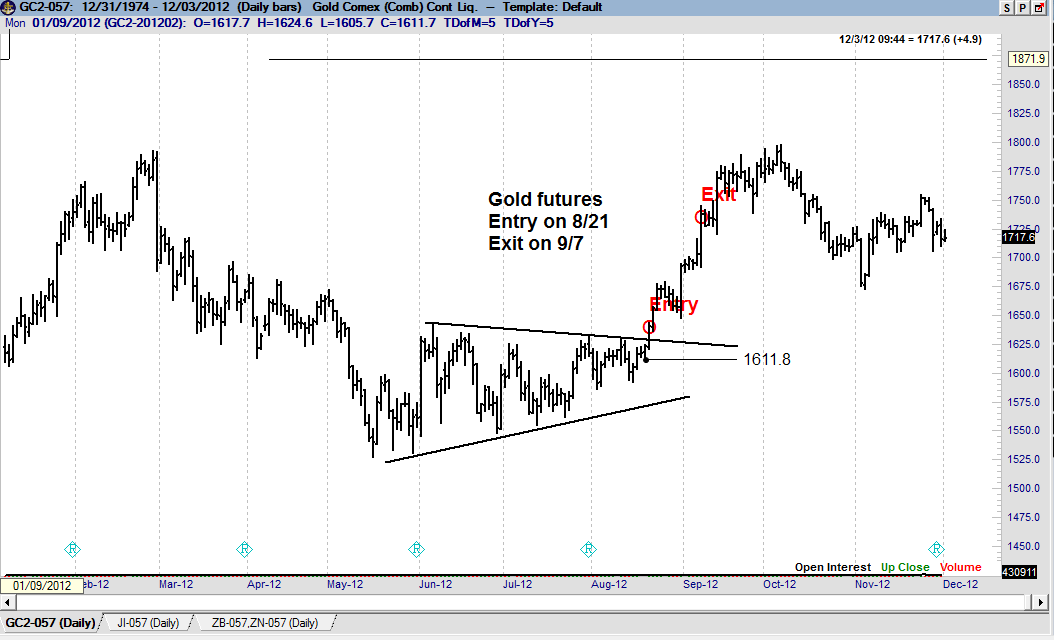

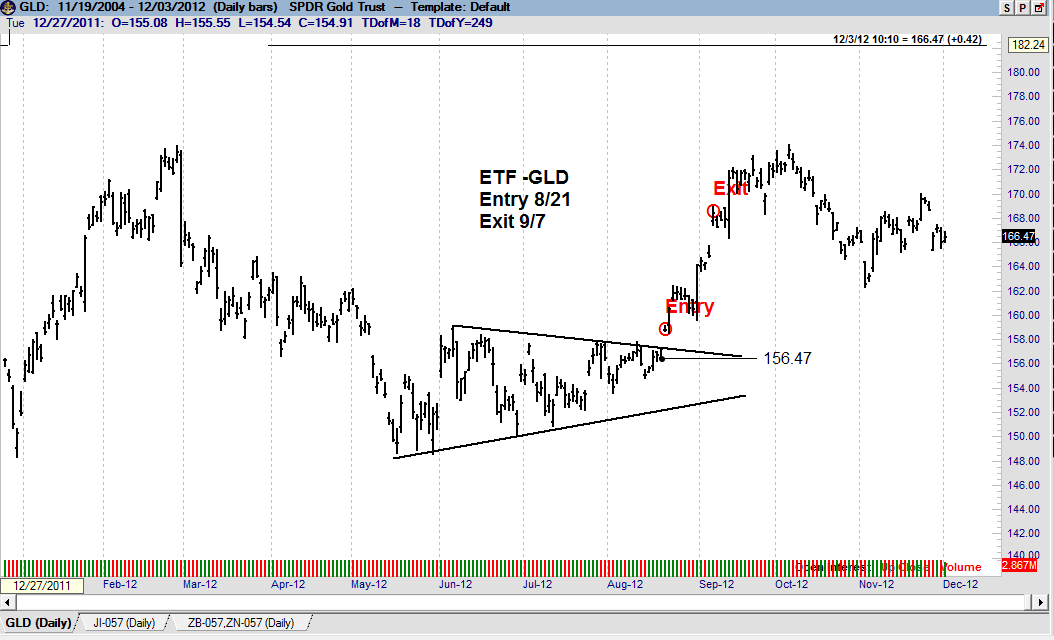

Summary: Trading a long Gold ETF (GLD) ties up nine times more capital in a trade with a near-identical risk to reward profile. FOOLISH!

Summary: Trading a long Copper ETF (JJC) offered 25% more profit potential, but tied up eight times more capital in a trade with a near-identical risk profile. FOOLISH!

I could go on and on with these examples — to interest rate markets, grains, energy, food and fiber, every conceivable forex pair.

No matter how you stack it, using ETFs when underlying futures or forex contracts are available is an absolutely foolish utilization of trading capital.

With the sole of exceptions of having an account with too little capital to trade futures or an IRA or Roth account unable to use futures, why a person would trade GLD or SLV or SPY or any number of futures/forex-related ETFs in beyond my comprehension?

For the same risk per trade (expressed in dollars or as a percent of a trading account), futures/forex provide the following advantages:

If you are a properly capitalized trader (I would saying anything north of $100,000 of non-IRA trading assets) you need to seriously challenge your use of ETFs instead of the underlying futures contract or forex cross.

PLB

###

I have a theory about the U.S. stock market (and all other markets). I have no idea if I am right or wrong, but I believe with all my heart I am right.

The theory is that there is only one major fundamental or global macro factor (at the outside, maybe two) that drives a major trend in the U.S. stock market. I call this theory the “Dominant Fundamental Factor.”

All the other apparently important fundamental factors just create confusion and market noise.

All day long we witness market “experts,” brokerage firm research analysts, the talking heads on CBNC and Bloomberg and participants in social media (Twitter, private chat rooms, et al) present this fundamental data or that fundamental data as the factors they feel should be driving market prices. In 95% of the cases, the fundamentals presented by these voices are unimportant — the facts may be correct, but the fundamentals behind the facts presented are not “market drivers.”

Traders and analysts develop the opinion that the things they focus on are really important drivers of price.

Some analysts believe that the market is driven by the composite of all the above factors and more — it is their job to put all the pieces together.

To the above idea, I say B___ S___!

History shows us that major trends in the U.S. stock market are driven by a Dominant Fundamental Factor — and that all the other fundamentals were throw aways during the course of said trends.

The challenge is to figure out what the Dominant Fundamental Factor is for a major trend — and to stay focused on it. The difficulty comes about because the next major trend will be driven by a different Dominant Fundamental Factor.

In the meanwhile, most traders and “talking heads” are pursuing knowledge of things that just do not matter.

Think about it:

The market decline in Oct 2007 – Mar 2009 was driven by the mortgage crisis and related economic fall-out. Nothing else really mattered. The mortgage crisis was the Dominant Fundamental Factor. Focusing on anything else paid no dividend and only caused confusion.

The market turn-around from Mar 2009 through late 2011/early 2012 was driven by QE. A tidal wave of cash infusion overwhelmed every other global macro or fundamental element. QE was the Dominant Fundamental Factor. Focusing on anything else paid no dividend and only caused confusion.

The bull advance in U.S. stocks from early 2012 through late 2014 was driven by corporate earnings — and this was the Dominant Fundamental Factor. Focusing on anything else paid no dividend and only caused confusion.

I am not sure if there has been a Dominant Fundamental Factor driving the market from late 2014 through the present day — or perhaps, two Dominant Fundamental Factors have cancelled each other out (trend to NIRP vs. debt de-leveraging).

So, what will be the next Dominant Fundamental Factor. I am not sure, but I am sure of is this:

I, for one, post many graphs and charts on Stock Twits and Twitter showing reasons why the U.S. stock market should be responding in a certain way. Yet, if the data shown by the graphs do not represent the Dominant Fundamental Factor, then the data is just noise. The graphs are still interesting fodder, but they do not have any real importance.

This brings me full circle back to why I am a chartist. I am not smart enough to determine what the Dominant Fundamental Factor is at any given point in time. I do not have the knowledge of global macro factors to make this determination. But, I trust that the charts will show me the way — and that I will learn of the Dominant Fundamental Factor after the fact.

Perhaps the Dominant Fundamental Factor beginning to play out is the global chase for yield. This is a possibility. If so, this will nullify all other global macro considerations.

Many very smart people are pointing to the eventual outcome of global NIRP. We have never had negative interest rates like we are experiencing. There will be a huge price to pay for the reckless endeavors of global central bankers. Eventually the side effects of NIRP will be the Dominant Fundamental Factor. But I do not know when, or how things will play out.

Anyway, that is my two cents — and that is what my opinion is probably worth.

plb

###